When we hear the phrase “Trusted Advisor,” most of us think of external experts: consultants, actuaries, accountants, lawyers, the professions. But there is another group for whom that term is at least as relevant—maybe even more so. That group is made up of internal staff functions: and mainly the “Staff Big Four:” HR, IT, Legal and Finance.

These internal staff have exactly the same challenge that their outside brethren have—to successfully persuade and influence others, over whom they have exactly zero direct authority.

But it’s worse for internals: first, because they eat in the same lunchroom as their clients and are known by their first names, they tend to not get the same respect that outside experts do.

Second: an internal consultant can’t fire his or her client. They are joined at the hip, like a married couple, for better or worse.

The Big 4 functions represent a big chunk of our business, not far behind trusted advisor work, and about the same level as Trust-based Selling work. And although the keys to success are pretty much the same for internal advisors as for externals, there are some distinct cultural problems that each of the Big 4 functions face.

Differences Between the Big 4 Functions

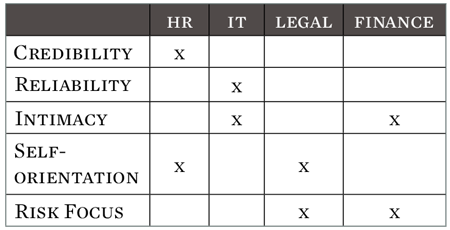

- The IT Challenge. Ask any line employee. “The problem with IT,” they’ll say, is “they use too much jargon and don’t deliver on time or on budget.” Strip out the value-laden words and what we hear is that IT has a reputation for being non-user-friendly, and that its big trust opportunity may lie in improving reliability.

- The HR Challenge. Unlike their IT brethren, HR suffers from speaking the same language as everyone else; which means everyone else feels equal to them in expertise. AS HR folks will tell you: “they can’t get no respect;” and they more they ask for it, they less they get.

- The Legal Challenge. You know this one too. “The trouble with lawyers is, they always tell me what I can’t do, and don’t help me with what I can do.” Let’s translate that into simply a predilection for avoiding Type 1 error (doing the wrong thing) at the cost of Type 2 error (not doing the right thing). Let’s call this one a misalignment around risk profiles.

- The Finance Challenge. Finance tends to speak clearly, meet deadlines, and be very sober about risk. In fact, very sober about pretty much everything. The fear that clients have of finance people is that of being relentlessly ground down on budgets, financial analyses, plans and forecasts. They are relentlessly, somberly, right.

Each of these groups can take some simple, solid steps toward improving their level of trust by their clients. (And if you’re an external, keep reading: this applies to you too).

Key Trust Opportunities by Function

Improving Credibility. More an issue for HR than the others, remember that credibility is not only—in fact, not even mainly—an issue of credentials. The average internal client is not impressed that you have advanced degrees, or that you are a recognized expert in OD. You can argue that’s not fair, but arguing fairness just digs the hole deeper.

What improves credibility is the capacity to apply your knowledge to a specific client situation—in their language. Instead of letting the client know that you’ve seen the latest, greatest research on teaching emotional intelligence—instead, use emotional intelligence yourself to help identify, and identify yourself with, client issues. For example, “Joe, do you find your people are as involved in work as you’d like them to be? Where do you see that playing out? And how big an issue is it for you? In what terms?”

Improving reliability. Reliability—an issue that affects IT more than the other Big Four—is one of the four key components of the Trust Equation, and one of the easiest to correct. Simple awareness is a good place to begin. Reliability lends itself far more easily to measurement than do the other components of trust (credibility, intimacy, low self-orientation); figure out good measures of reliability, and track them. Think you’re already doing the most you can? Try increasing the number of promises you make, even small ones; then make sure to meet them.

Improving Intimacy. Intimacy is the variable that makes an advisor ‘client-friendly.’ Intimacy skills are what make a client feel comfortable sharing, or not sharing, information with you. If you’re being constantly shunted into a role which is far short of your capabilities, this is one area to focus on (the other is self-orientation—see below).

You don’t have to resort to commenting on kids’ pictures, college degrees and ‘how ‘bout them Bulls.’ Make it a point to learn things about your clients’ business lives—then ask them for help in understanding things that you genuinely don’t understand about them.

Self-Orientation. We find that nearly everyone can improve their trustworthiness by getting better at lowering their self-orientation (see “Get Off Your S”). Within the Big Four internals, this is particularly useful for HR and IT organizations. Too many clients see HR as whiney, and lawyers as officious: both of which are forms of overly developed self-orientation.

The solution is harder than for the other issues, but well within reach. Simply be very, very sure to see issues from the client’s vantage point—not just from yours. No one’s asking you to abdicate your professional perspectives, just to see it as well from the other side of the table. If a client says to you, “We want to do X, how can we do it?” make sure to start with, “Interesting idea; let me make sure I understand what this means to you. Tell me more about what you could do with this, how it would make you more successful. I want to make sure I know where you’re coming from before I try to comment.”

Risk-Orientation. Both Finance and Legal get heavily tarred with the brush of being too risk-averse. To some extent that may seem unfair; after all, part of their job is indeed, to manage downside risk.

But organizations that adopt an adversarial relationship, where Legal represents the downside and management argues for the upside, are creating vast areas of unnecessary cost, mistrust and confusion. It’s far better to create collaborative relationships, where issues can be sorted out mutually.

While improving self-orientation and intimacy skills are certainly relevant for many legal and financial people, there is still an underlying disconnect about risk. This disconnect has to be called out at the start. It’s no good having lawyers and Finance people suggesting, from the get-go, that their role is to reign in the irrational exuberance of those id- and ego-driven people out there in the market; we can look at the pharmaceutical and investment banking industries as pockets where the relationship has deteriorated into such a caricature, and it is not pretty.

Instead, staff people have to state the terms at the outset: ‘We are here to collaborate with you in jointly determining the right amount of business risk to take on, consistent with legal, regulatory and market-based risk. We all work for the same organization; and we’re committed to working with you.’

Then, walk the talk.